1

Question 1 of 15

When economic principles are developed from factual evidence, this method of economic reasoning is called

This A Level Economics Quiz 2015 Part 1 quiz contains 15 multiple choice questions designed to help you revise and test your A level Economics Quizzes knowledge. Select an answer for each question and click “Submit Answer” to see instant feedback. Take your time and try to score as high as possible!

Economics as a whole is a social science subject concerned chiefly with description and analysis of the production and distribution of goods and services. This subject also deals with the studies of how individuals, governments and nations make decisions about how to allocate resources.

In this quiz, we shall examine questions that are based on the following topics: “market economy, factors affecting population, demand and supply and so on”

In order to help out with your studies in economics, we have selected 15 questions from the June session of 2015. These questions will give you a general view of how the exam questions are set and how one can reason out to answer the questions. These questions are based on the CGCE Advanced level Economics. Each question has four options and only one is correct among these options. In addition to these quizzes, there are other quizzes available which are also based on past CGCE past questions.

Good Luck

Question 1 of 15

When economic principles are developed from factual evidence, this method of economic reasoning is called

Question 2 of 15

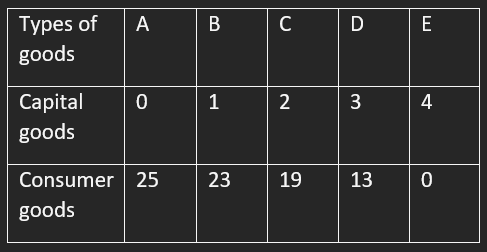

Question 2 is based on the table below, showing the production possibility situation of a country

If this economy chooses the combination of goods at point A,

Question 3 of 15

A market economy can result in

Question 4 of 15

Which of the following will likely trigger a move from a command economy to a market economy?

Question 5 of 15

A security whose market price is the same as its nominal value is said to be

Question 6 of 15

If the quantity of all factors used in a production process increased by 10% and production rose by 15% there are

Question 7 of 15

Providence and Son’s enterprise has a capital structure composed of:

Debentures - 40 million FCFA

Preferences shares - 80 million FCFA

If the company is lowly geared, the figure for

its ordinary share capital might be

Question 8 of 15

If an industry remains in an area long after the factors that attracted it have disappeared, this is known as

Question 9 of 15

Total population = 100 million people

Birth rate = 5 per thousand

National growth rate = 2 per thousand

The number of deaths in this population is:

Question 10 of 15

Total population = 100 million people

Birth rate = 5 per thousand

National growth rate = 2 per thousand

An ageing population will result in

Question 11 of 15

Total population = 100 million people

Birth rate = 5 per thousand

National growth rate = 2 per thousand

Under which of the following circumstances would an increase in the price of good X result in a fall in the demand for good Y?

Question 12 of 15

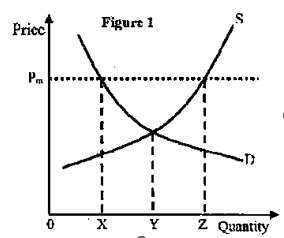

If the government of a country fixes a guaranteed minimum price of Pm the effect would be that

Question 13 of 15

A given industry supplies 3,000 units of a good per month at a price of 40 FCFA per unit. If the price elasticity of supply is 4, how many units will this firm supply if the price rises to 50 FCFA?

Question 14 of 15

Given a market demand curve Q=120-2P and supply curve Q=4 P, where P represents price, the equilibrium quantity and price are

Question 15 of 15

A shift of a demand curve to the left could be caused by:

Economics is a branch of social science that studies how individuals, house...

Economics is the study of how humans make decisions in the face of scarcity...

Economics as a social science subject is the scientific study of the owners...

A Level Economics Quiz 2016 Part 2 Economics is often defined as the study ...